TOGETHER WITH  | Good Thursday to you. Can you guess what's the average cost to hire a handyman in the US for a typical project? a. $17, b. $70, c. $170. Follow the wave 🌊 below for the answer. Here are our money and housing-related topics for today: - Getting equity rich

- Looking to buy a home? A look into those mortgage rates

- The cost of working from home

| |

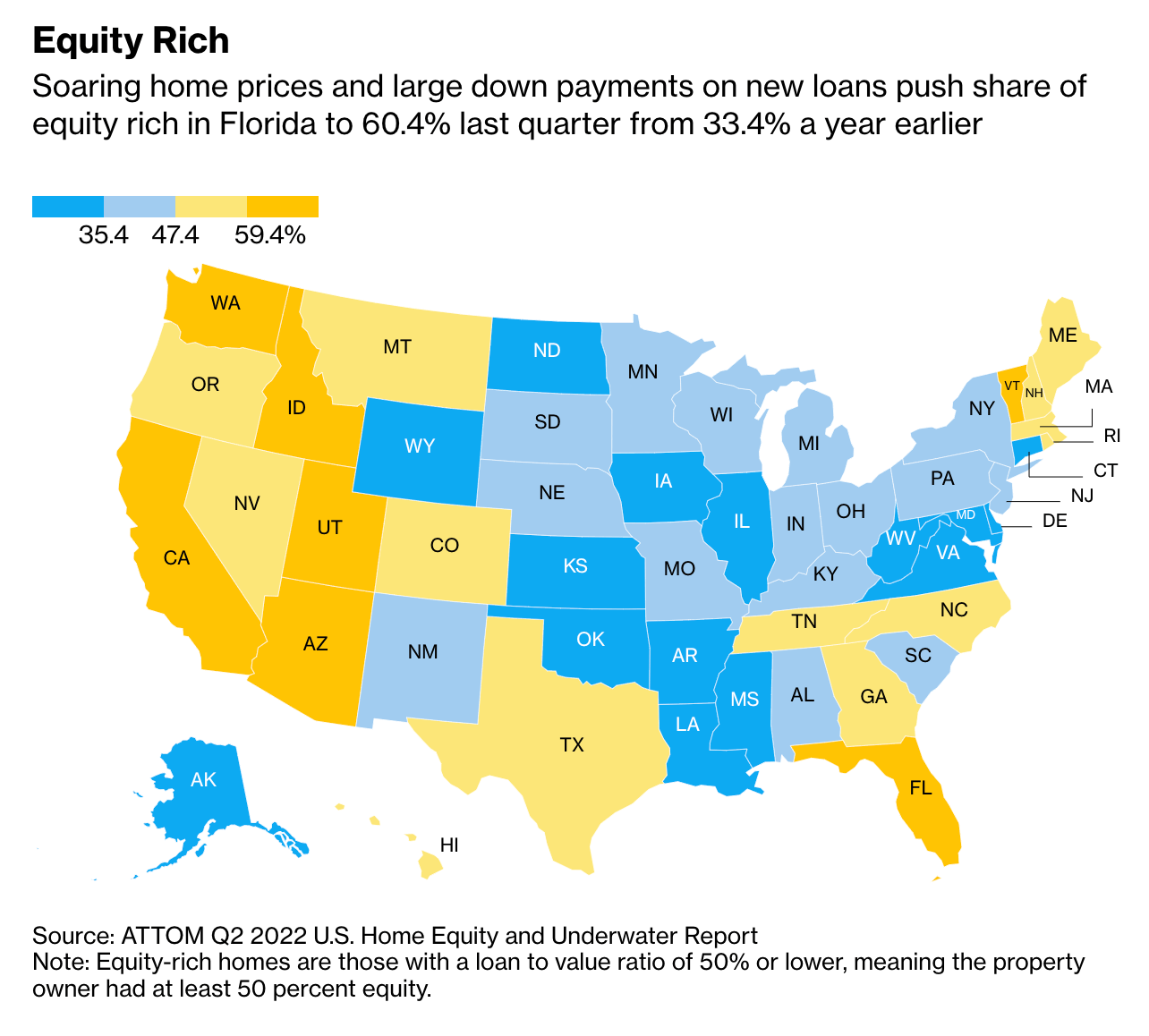

HOUSING MARKET Getting Equity Rich | | | | There’s been a lot of negative talk around the housing market and its astronomic prices over the last twelve months, but as they say, there are two sides to every coin. Although rising prices are bad for those looking to buy, they’ve been a massive blessing to those who have already bought, and the numbers are astounding. A new level of wealth - Climbing still: The most recent data shows that the median sale price was higher in Q2 of 2022 than Q2 of 2021 for homes in 184/185 metro areas monitored, up 14.2% to $413,500. That increase resulted in a 10% or higher increase in 80% of cities tracked, and this continued trickle northward is what’s creating this equity wealth.

- Equity rich: In Q2 of this year, almost 50% of homes with a mortgage were considered “equity rich,” meaning a homeowner had amassed at least 50% equity in their home.

- Continuing to rise: This is a perpetuation of the same trend we’ve been seeing for two years now. While nationally, 48.1% of mortgaged homes were equity rich in Q2, this is up from 44.9% in Q1, and 34.4% one year ago—leading to more evidence that home valuations have continued to rise amidst these rate hikes.

- A rising tide lifts all boats: The same is true on the opposite end of the spectrum, just in a different way. The number of mortgaged homes underwater has also dropped to a low of just 2.9%, down from 4.1% one year ago.

Going forward? Home price growth is slowing, but a far cry from declining. In the meantime, homeowners are continuing to accrue equity and the market finds itself at an apex of sorts where growth is dampened, but the next move is still uncertain. For those owning a home, it might be wise not to be too brash with that equity, and to avoid making any risky moves while valuations settle out. And for those house hunting, it looks as if that historic growth trend is turning in your favor... for now anyway. Take this related lesson on this topic and earn Dibs 🟡 while you're at it

| | | |

MORTGAGE RATES Looking To Buy A Home? | | | | Much has been made of the ramifications felt as a result of the Fed’s rate hikes this year, and mortgage rates have perhaps been the biggest, most costly victim of those increases. And yet as quickly as they rose, rates have now fallen back down again. If you’re a serious buyer who doesn’t believe in waiting when it comes to homeownership, now might be a ripe time to lock in a loan. Wait, what happened? - Where are we now? The average rate on a 30-year fixed mortgage hit a 13-year high of 5.81% in June but has since fallen to now hover around 5% or so, depending on your lender and credit situation.

- Why did rates fall? The next time someone asks you the exact science of how mortgage rates are set, you’ll understand why your parents used to answer questions with “it just is.” It’s complicated, and although the rising Federal Funds rate did push them up, lenders also account for many other business factors and economic projections. Recent concerns about slowing growth and inflation have contributed to the drop.

- A lot of movement: Rates have become relatively volatile lately as lots of catalysts weigh on their calculations. The housing market, and subsequently the lending side too, seems to very much be in a state of rebalancing as it searches for a new normal.

Benefitting from this - Growth and sales: As of June, sales of previously owned homes had fallen for a fifth straight month—overall price growth is slowing in many markets across the nation. While this isn’t exactly like a Christmas miracle or anything, we can acknowledge that higher rates have contributed to this, and hope it’s kicked off a new trend in a more affordable direction.

- Getting creative: Rate volatility has given way to a spark in the world of refinancing too, as many recent buyers are likely vying to lock in a lower rate. One easy way to avoid this hassle is by opting for an adjustable-rate mortgage (ARM) which allows you the opportunity, and the risk, of riding current rates. Simply put, ARMs are home loans with a variable rate—usually after an initial fixed period of time. And their rates fluctuate with the market, adjusting on a yearly or monthly basis. They’ve become increasingly popular recently, and of course, you could always refinance once rates reach a more desirable point.

Take this related lesson on this topic and earn Dibs 🟡 while you're at it:

| | | |

SPONSORED BY ALLIO Do More With Your Money | | | | What if saving was actually easy & automatic? Allio is an all-in-one solution you can use to start saving and achieving your financial goals, regardless of how much money you have in your budget. Whether you want to set up a recurring investment, opt into round-ups that let you automatically invest as you make everyday purchases, or simply make one-time deposits Allio has you covered. Do more with your money, with Allio. Join the waitlist today. | | | |

MONEY TIP The Cost of Working From Home | | | | Working from home can save most employees and business owners a lot of money. Without the cost of transportation, buying occasional food, and even spending less on clothes, the savings add up pretty quickly. That’s not the case for everyone though because spending more time at home can actually result in higher expenses each month if you’re not careful, especially when it comes to that energy bill. How is that so? - Increased activity: Studies conducted in 2020 found that residential usage rose about 5% as people spent more time at home, using its amenities. From April to July 2020, Americans in aggregate paid about $6B more on their electric bills than they would have in a typical year.

- Changing patterns: Electricity usage is known for seeing its peak hours during the morning and evening times, often associated with your typical 9-5 or school schedule. During the pandemic, though, we saw those peaks flatten out a bit as consumers started using more electricity throughout the day. This impacts the bill because many providers consider these to be “peak hours” which make electricity more expensive per kilowatt hour used.

- Uneven implications: These impacts have been found to disproportionately impact minorities and low-income families, often because they live in older, less efficient homes, with less efficient appliances, less efficient heating and air, or in older neighborhoods with less efficient power grids.

Take this related lesson on this topic and earn Dibs 🟡 while you're at it:

| | | |

🔥 TODAY'S MOVERS & SHAKERS | - Walmart (+5.2%) shares are up after reporting better-than-expected Q2 earnings results; the retail giant also shared this morning that higher-end shoppers are walking its aisles while regular shoppers are downgrading to generic brands.

- Ally Financial (+3.1%) as it's been revealed that Warren Buffet's Berkshire Hathaway tripled its investment in the online banking company in Q2.

- Ziprecruiter (-7.2%) despite beating Q2 earnings thanks to the strong labor market. However, the online recruiting company expects a slow down as companies are pulling back on open positions.

- Bitcoin (-1.1%) to $23,825.10 (1D)

- Ethereum (-0.7%) to $1,885.59 (1D)

This commentary is as of 8:30 am PDT. | | | |

🌊 BY THE WAY | - 🛠️ Answer: $70, that's the US national average spent on a typical handyman service. And, here's more: a housecleaner is $200, a plumber is $150 and a lawn professional is $60 (Thumbtack)

- 👩🏻🔬 Walgreens is paying signing bonuses up to $75,000 to pharmacists (CNN)

- 💰 ICYMI. Things to remember before tapping into your home equity (Finny)

- 🥝 The clean 15: Non-organic fruits and veggies that are safest, least toxic to buy (Medical Daily)

- 🍋 Homeowners insurance top-rated by people and big banks. Rated 4.9/5 stars in the App store. Get the home insurance trusted by all major lenders (Lemonade*)

- ☂️ Finny lesson of the day: Another home-buying cost to take into account is home insurance. Get the skinny on the basics and how much you should expect to pay for it:

| | | |

What did you think of Finny's The Gist today? (Click to vote) | | | |

| Finny is a financial education platform on a mission to make your money work for you. We offer a customized financial learning platform through bite-size, jargon-free lessons, money trends & insights. The Gist is Finny's twice-a-week (Tues & Thurs) newsletter covering personal finance & investing insights and money trends. Finny does not offer investment and stock advice or endorsements. The Gist content team: Chihee Kim, Austin Payne, Carla Olson. We're thankful for the support of today's sponsors & partners*—Allio, Lemonade—as they make rewards on our platform possible. If you're interested in sponsoring The Gist, please reach out to us. And if you have any feedback for us, please contact us. | | | | | | | |

No comments:

Post a Comment