TOGETHER WITH  | Good day. Can you guess how many of the roughly 500 companies in the S&P 500 index cited the term “recession” in their Q2 earnings calls? a. 140, b. 240, c. 340. Follow the wave 🌊 below for the answer. Here are today's money topics: - The state of the 60/40 portfolio

- Retail traders have lost some power

- Take advantage of all your employee benefits

| |

INVESTING The State of The 60/40 Portfolio | | | | The 60/40 portfolio holds 60% stocks and 40% bonds. The concept was coined by Vanguard’s founder, John Bogle, and has been considered a tried and true allocation for many decades now. The reasons for its existence come down to simplicity, reliability, and good returns. It’s a more extreme example of something like the rule of 110, which says your equity allocation should be 110 minus your age. For example, if you’re 30 years old with a moderate risk profile, you would hold 80% in stocks or stock funds (110-30 years old = 80% stocks). - The returns speak for themselves. The main goal of a 60/40 portfolio is to reliably deliver average returns of around 7% annually. But this asset mix has actually averaged 8.8% between 1926 and 2021, 11.5% since the financial crisis, and generated positive returns in 35 out of the 42 years since 1980. Batting .833 ain’t too bad.

- But it has its haters: Despite having one of its worst years in a while, headlines claiming the 60/40 portfolio’s death have been vastly overstated. As of Sept. 7th, the portfolio’s return this year sits at a dismal -17.25%, but this down year doesn’t discount its viability going forward.

- A weird scenario: Alternatively, a portfolio allocated 100% to the total stock market would be down about 17.23% this year, which is quite literally no different. The problem is that bonds are usually expected to have an inverse relationship to stocks, and because of rising interest rates this year, the price of existing bonds has fallen, eliminating the 60/40 portfolio’s usual 40% bond hedge.

- All is not lost though: The 60/40 remains a classic, reliable default portfolio that we should reasonably expect to continue its relatively predictable performance going forward, even if it does have a blip like 2022 here and there. It’s not the gospel of investing though, and we should always use our risk tolerance, time horizons, and financial goals to arrive at the right allocations for ourselves.

Take this related lesson on this topic and earn Dibs 🟡 while you're at it:

| | | |

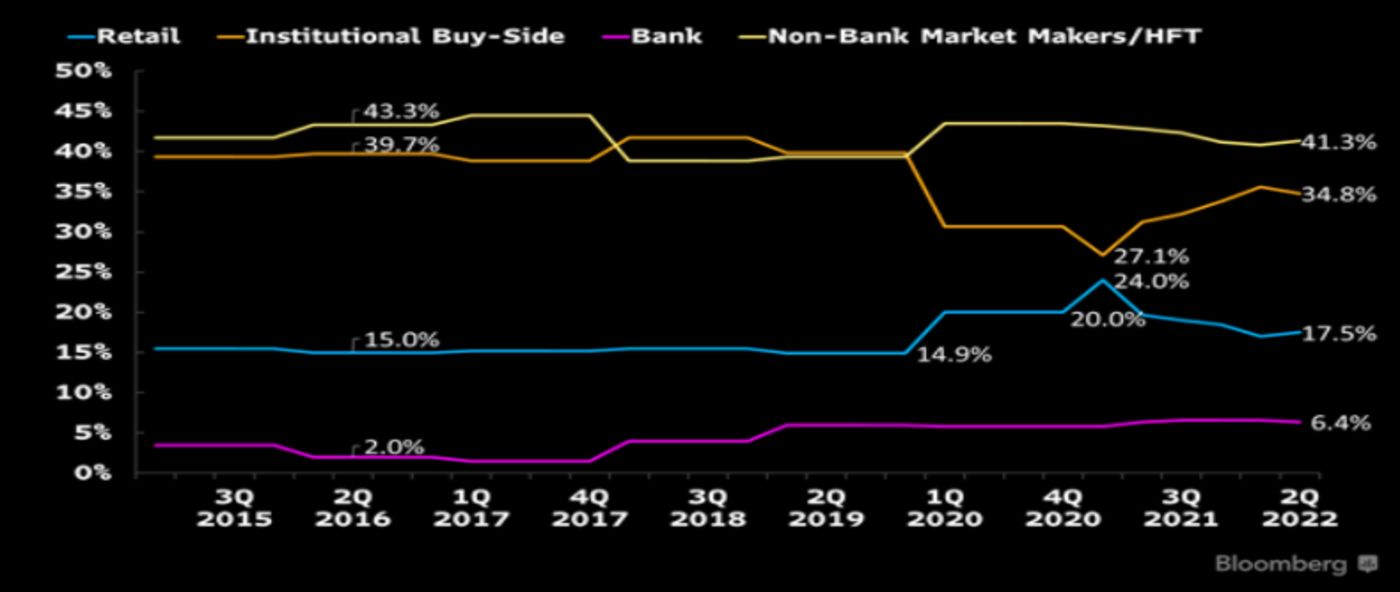

MARKET OUTLOOK Retail Traders Have Lost Some Power | | | | The end of 2020 rolled seamlessly into 2021 with a common trend intact: Retail traders exerted a never before seen influence on the markets. Between well-known escapades like Gamestop and tens of lesser-known meme stocks that retail traders turned into multi-baggers, these investors were throwing their weight around for once, to the point that the SEC even investigated it. But what goes up, must come down - A measurable presence: The meme stock frenzy wasn’t just an anecdotal experience that was seen culturally, locally, or online, but in the numbers too. Retail traders made up 24% of all trading activity back in Q1 of 2021, an all-time high.

- Getting humbled: This was followed by a harsh drawdown in Q2 of last year that knocked retailers back, but the underlying effort was still there. Since then, trading volume consumed by individuals has dwindled, falling back to 17.5% by Q2 of 2022.

- A dragging trend: Meme stocks and the retail movement isn’t “dead” per se, but it is dragging. Despite a July/August bounce that did take some momentum plays with it, the overall trend is down. Trendy plays have fallen all around, and funds centered on this idea are hurting too, with popular ETF $MEME being down a whopping 53% YTD.

Trading volume breakdown by market participants

Source: Bloomberg Intelligence

It’s not all bad news though Individual participants are still making up more of the market than ever, and a decline to 17.5% of transactions is still steadily above the 10-15% we’ve seen traditionally. Meme stocks are probably harmless, but we know they’re unsustainable. It’s all part of a broader shift toward giving individuals the power to play and taking the power out of the hands of those who were traditionally privy to the markets. Basically, we’re getting rid of the middlemen. Take this related lesson on this topic and earn Dibs 🟡 while you're at it: | | | |

SPONSORED BY MASTERWORKS Beat the “Decade of Lost Wealth” with One App | | | | The stock market is down 20%, its worst first half since 1970. Inflation sits at 8.5%, its highest in 40 years. Now, economists say there's a 50% chance of a severe recession. How can you prepare? For centuries, the ultra-wealthy have insulated their wealth through an exclusive, multi-trillion dollar, alternative asset: fine art. In fact, in the last quarter-century, contemporary art prices have outpaced the S&P 500 by a staggering 164%. With Masterworks, everyday investors can now access the top-end of the art market by buying shares of iconic artworks by names like Picasso and Banksy. In their last 6 exits, Masterworks has realized an average net return of 29.0%*. Due to record demand, shares of some paintings have sold out in just 14 minutes. But readers of The Gist can get in on the action by skipping the waitlist via this exclusive referral link.

| | | |

WORK BENEFITS Take Advantage of All Your Employee Benefits | | | | High-quality employee benefits are something all of us long for when sorting through potential employers. And as we should, these add-ons can make a massive difference in our finances both long and short term. Unfortunately, sometimes we often take them for granted, overlook a couple, or simply don’t maximize the options offered to us. Tips to take full advantage - Max your match: If your employer offers a 401(k) match, taking advantage fully is the best thing you can do. It’s free money, after all. If you have a 50% on-the-dollar match for up to 6% of your $50k salary, that’s a potential extra $3k per year. If you only contribute 3%, you’re missing out on $1,500 every year, or $30,000 over 20 years. If you broke this extra cash down to investing $125 per month in an S&P fund, that would amount to $66,403 after just 20 years. Don't miss out on all that compounding, free money!

- Schedule time to explore: Understanding all your benefits becomes increasingly important if your company offers many benefits. It’s a good problem to have, so taking the time to explore your HR portal or just talking with your HR department and reviewing your documents can go a long way and save you tons of money.

- Pricing benefits: Many employees will have an array of benefits and perks that are huge money savers. For example, you can get a full estate plan through a monthly legal subscription service, free or cheaper insurance services (i.e., group life, pet, etc.), and even access to a wide range of mental, health, and financial wellness services at no cost.

| | | |

🔥 TODAY'S MOVERS & SHAKERS | - Adobe (-17.1%) shares fall on the announcement it will acquire design platform Figma for $20 billion in cash and stock.

- Store Capital Corp (+20%) on news that the REIT will be acquired by GIC, a global institutional investor, and funds managed by Oak Street in an all-cash transaction valued at approximately $14 billion.

- Rail stocks are higher on reports of a tentative agreement preventing a rail workers' strike; Union Pacific (+2.4%), Norfolk Southern (+1.6%).

- Wynn Resorts (+8.7%) as its stock was upgraded by Credit Suisse, calling the casino/resort operator "one of the most compelling stories in the gaming industry."

- Bitcoin (-2.6%) to $19,699 (1D)

- Ethereum (-9.6%) to $1,481.79 (1D)

This commentary is as of 8:30 am PDT. | | | |

🌊 BY THE WAY | - 📢 Answer: 240 companies within the S&P 500 cited the term “recession” during their most recent Q2 earnings calls, which is well above the 5-year average of 52. The term "inflation" was cited by 412 S&P 500 companies and "supply chain" was mentioned by 325 S&P 500 companies on those recent calls (FactSet)

- 🔀 Ethereum's energy-saving merge is complete (Bloomberg)

- 🔋 Biden announces first round of funding for EV charging network across 35 states (CNBC)

- 🚑 ICYMI. Bear market survival tips (Finny)

- 🧑🏽⚖️ And while we're on EV, Nikola founder Trevor Milton stands trial on fraud charges, capping a stunning rise and fall (CNBC)

- 💧 Oh, and Kellogg’s wants you to add water to its new cereal (CNN)

- 📄 Finny lesson of the day. While it's good to know what kinds of benefits your work offers, it's also good to understand what gets taken out of your paycheck, why, and what changes you can make:

| | | |

What did you think of Finny's The Gist today? (Click to vote) | | | |

| Masterworks Disclosures *Net est. returns for all realized and unrealized offerings 15.3%, from inception through 6/30/22. See important Reg A and performance disclosures. About Finny Finny is a financial wellness platform on a mission to make your money work for you. The Gist is Finny's twice-a-week (Tues & Thurs) newsletter covering personal finance & investing insights and money trends. The content team: Austin Payne, Carla Olson, Chihee Kim. Finny does not offer investment and stock advice or product endorsements. We're thankful for the support of today's sponsor & partner—Masterworks—as they make rewards on our platform possible. If you're interested in sponsoring The Gist, please reach out to us. And if you have any feedback for us, please contact us. | | | | | | | |

No comments:

Post a Comment