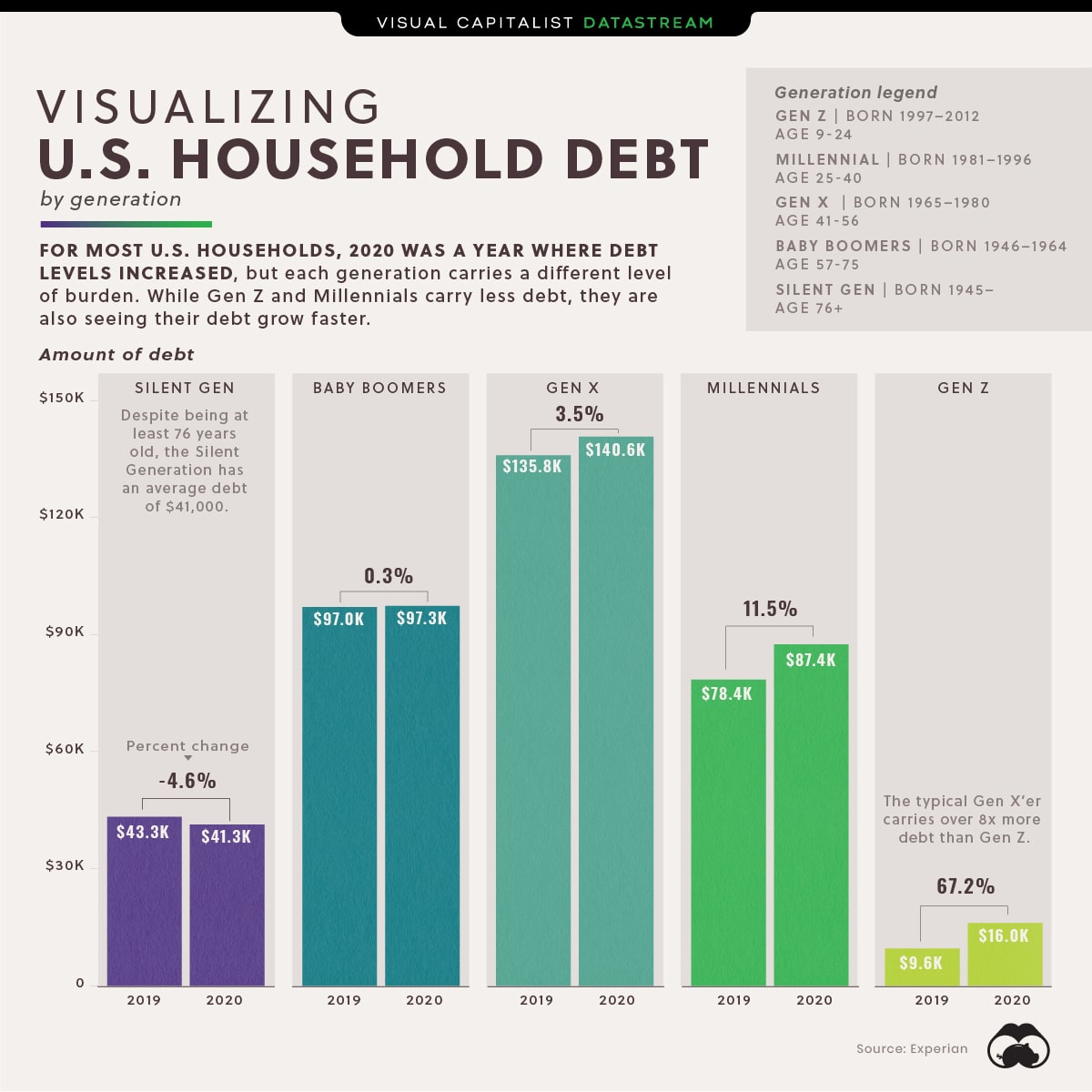

| Debt makes the world go round. Okay, more like the economy and modern life, but you get the gist. It's because of debt and the debated fractional reserve lending system that we're able to start a business, buy a car, or get a mortgage. For better or for worse, debt kind of runs the country. Debt can be a good investment when it's owed to you, and not always when you owe it. Although household debt doesn't get 'passed down' in the most traditional sense, the proverbial financial burden of debt placed in each subsequent generation is something that's been increasing over time. It wasn't always this way Debt hasn't always been as conveniently accessible as it is today. Credit cards didn't exist until 1950, most Americans didn't even own a car up until that time, student loans owed by graduation have increased by 326% since 1970, and mortgage debt has increased exponentially over the last 70 years. Fun fact: In 1862 the US government actually gave away 270 million acres of land with Lincoln's Homestead Act. That came out to about 160 acres of land per family that could be passed down over generations, without a loan. In 2021, essentially all land is accounted for. Things haven't always been this compartmentalized and debt-oriented. So, the generational debt snowball grows According to data from Experian, Generation X is at its peak debt-saddled stage of life right now, holding an average household total of over $140,000 each, mostly consisting of mortgages. Behind them are the Baby Boomers, who average a $97K per household number made up of again, mostly mortgage debt, but growing at a lesser rate. Millennials are an average of $87K in the hole, but that number is growing at the second-highest rate amongst the generations, and it's reasonable to expect this age cohort to someday outdo Gen X. A large portion of their debt is consumed by student loans and credit card debt, as is the case with Gen Z, who despite their low total of $16K, saw their debt jump by 67% from 2019-2020.

Source—Visual Capitalist, US Household Debt, by Generation What do we do with this information? Some things are just interesting to know and nothing more, but there is one takeaway we can glean from this data, and it's being aware of how easy it is to fall deep into debt. Not all debt is bad debt, but even good debt can go bad if mismanaged. So we should be exceedingly cautious about taking on more liabilities. Think twice about paying that tuition just because it's been a dream school, make sure that mortgage isn't 50% of your income and maybe don't use that credit card on the new iPhone 13 just yet. We can't control the financial system, but we can control our personal finances. 💳 New to managing your debt and want some insights that can help you plan your way out of it? Take this lesson: |

No comments:

Post a Comment