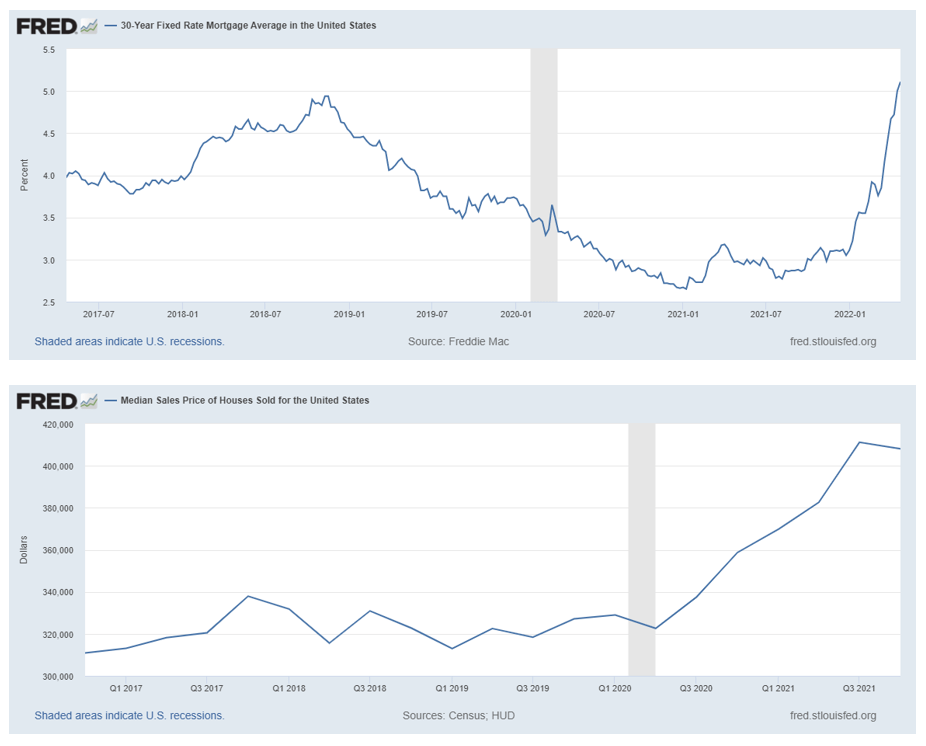

| Time in the market beats timing the market, right? Or wait, no, that’s the stock market. Does that apply to the housing market too? As we watch the cost of buying a home go through the roof, and the affordability out the window, it’s hard not to ask, should we just try to wait it out? Conditions have been ripe for home prices to spiral these last few years, and spiral they did, rising 20% since 2020 alone. Now though, the winds are shifting a bit, and prospective homebuyers can sense a potential shift in the market. The perfect storm—how it got this way - Interest rates: Home prices had been relatively flat, even falling a little, since their near-term peak in 2017, and they shot straight up as soon as the rates fell in 2020. If we compare the two charts, the inverse relationship we know all too well shows clearly, and this undoubtedly contributed to the spiral.

30-yr Fixed Mortgage Rate (top) vs. Median US Home Sales Price (bottom) - Savings: Spikes in personal savings rates directly coincided with the stimulus checks sent out to most of the population, but there were likely other factors involved with people moving out to the country and the economy slowing down. Saving a few thousand dollars the government sends out isn’t enough to turn millions into house hunters, but it’s a supporting factor nonetheless.

- Supply/demand: Despite hosting about 16 million “vacant” homes, it’s fairly well known that the US also has a housing shortage issue in the millions as well, especially in the single-family area. Vacant homes that aren’t available for whatever reason don’t solve the problem, new construction does. Despite the fact that housing starts have been rising, existing home sales are also at or near all-time highs, and inventories take a while to catch up.

The deterioration, maybe. Just like when a hurricane weakens when crossing over land, the housing market has its own kryptonites too. Between white-hot prices, tapped-out buyers, and interest rates bouncing back with a vengeance, we might just get some relief eventually. So, should you risk waiting it out? That depends a lot on your situation. If you’re a pre-approved buyer in a healthy financial situation and are looking for a home to keep for decades, waiting will likely make little difference for you, because this is your home, not a commodity to flip. Prices may flatten, trickle up, or even fall these next few years, but that doesn’t matter much for you. The mark-up you might score by waiting might not even offset the rent you would pay in the meantime. As an investor though, it might make sense to wait, but again, it depends. If you’re vying to lock in your first property in a high-demand area before rates move higher, maybe don’t wait. But if you need to finance your down payment with debt, the added interest may not make the investment attractive for you now and waiting might produce a better deal. Rental prices may exceed mortgage payments and related costs— getting to cash flow positive is always nice. 🏠 Related lesson alert. If you're new to homebuying, here's another relevant lesson that covers a few insights on mistakes to avoid when buying a home: |

No comments:

Post a Comment