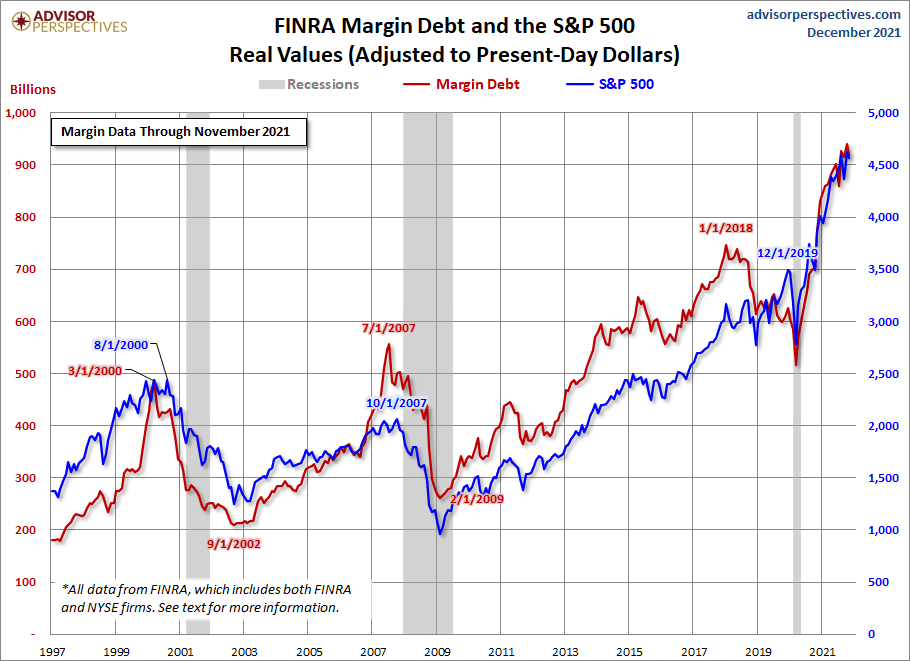

| Margin is a double-edged sword, one of many such weapons available for investors use and abuse within the financial world, and in the investing niche specifically. It can double your gains, and double your losses. It can amplify your bragging rights, or increase your debt exponentially. Whether or not you should indulge in this opportunity is a conundrum oft pondered by both newbies and seasoned veterans alike, because as lucrative as it may be, we know all too well that things that seem too good to be true always have drawbacks. Quick overview of margin Buying on margin means borrowing money from a broker to purchase securities. Think of it as a loan from your broker. It increases your purchasing power because you're using borrowed money to increase your financial leverage. Let's say you buy Apple stock for $200 and the price of the stock rises to $300. If you bought the stock in a regular cash account and paid for it in full, you'll earn a 50% return on your investment (i.e., $100 gain is 50% of your initial investment of $200). But if you bought the stock on margin—paying $100 in cash and borrowing $100 from your broker—you'd earn a 100 percent return on the money you invested (i.e., your $100 gain is 100% of your initial investment of $100), excluding the cost of borrowing the money. Margin investing has been around since the early 20th century and was actually first used to finance infrastructure like railroads. As we might expect, initial regulations were fairly loose, meaning it wasn't that uncommon to see accounts up to 90% leveraged. It's obviously come a long way from the roaring twenties and is now easier than ever to access. It's risen in popularity alongside the market over time, and the sustainability of these heightened brokerage debt levels is unknown.

The pros and cons to account for In a recent survey of 1,000 investors, 40% of participants said they'd made use of margin. 80% of GenZers said they'd taken on margin, compared to just 60% of Millennials, and an even lesser 28% of GenXers. That's a lot of leverage. The pros of buying on margin are obvious: amplified gains. As we saw in the example above, by trading Apple stock on margin, you could earn a 100% return versus 50% in a regular cash account. The appeal couldn't be more clear. The cons however are more numerous. Something often not accounted for when borrowing on margin is the fact that this is a loan with interest just like any other. Robinhood, for example, charges 2.5% on margin over $1,000. You can amplify your losses in a big way too. For example, let's say the Apple stock you bought for $200 falls to $50. If you fully paid for the stock yourself, you'd be down 75%. But, if you bought on margin, you'd lose more than 100 percent of your money (i.e, you're left with Apple stock worth $50, and after repaying your broker $100 for the borrowed money, you have -$50). In addition to the loss of your $100 initial investment, you would also owe your broker the interest on the margin loan and any other fees they may incur. |

No comments:

Post a Comment